The ISM has highlighted unmanaged procurement spend as a defining vulnerability for midsize organizations — one driven not by negligence, but by growth outpacing process. When vendor relationships are managed informally, buying decisions are made at the department level, and spend data lives in disconnected ERP and AP systems, the compounding cost is real: overpaid vendors, missed consolidation opportunities, and negotiating conversations you walk into blind.

This article covers the five spend management solution categories that matter most for mid-market companies, how to evaluate which ones fit your situation, and what separates organizations that build lasting savings capability from those that complete a single initiative and then revert.

TL;DR

- Spend management is an ongoing discipline: systematically gaining visibility into, controlling, and reducing third-party vendor costs

- Five core solution categories cover the full spectrum — from spend visibility and strategic sourcing to e-procurement automation

- Start with data before anything else — every downstream sourcing or negotiation effort depends on it

- Choose solutions based on procurement maturity, available headcount, and spend complexity — not just price

- The fastest path to results is often a hybrid model: small internal team sets strategy, specialized partners handle analytical and operational execution

What Is Spend Management — and Why Mid-Market Companies Get It Wrong

Spend management is the discipline of gaining full visibility into organizational expenditure, establishing control over purchasing decisions, and reducing costs without degrading supplier relationships. Unlike reactive cost-cutting — which tends to strain vendor relationships and erode service quality — spend management is a continuous, data-driven operating discipline.

Done well, it shifts procurement from a reactive function to a strategic lever that compounds over time.

The mid-market gap is structural, not accidental. Companies in the $100M–$2B revenue range typically outgrow the informal procurement practices that worked when they were smaller — handshake vendor relationships, department-level buying, no centralized spend data — but haven't yet built the processes and talent that make enterprise procurement functions effective.

What this produces in practice:

- Fragmented spend data spread across multiple ERPs, business units, and AP systems

- Unchecked maverick spending where departments buy outside approved channels

- Limited negotiating leverage because no one has consolidated data on total vendor spend

- Duplicate vendor relationships that inflate supplier counts and reduce volume leverage

Each of these gaps is solvable. The five solution categories below address them directly — starting with the analytics foundation and moving through the delivery models that give mid-market teams the capacity to act on what they find.

Top Spend Management Solutions for Mid-Market Companies

These five solutions are not competing alternatives. They represent complementary layers of a mature spend management program. Most mid-market companies start with visibility and build outward from there. Selection should be driven by your current team capacity, data maturity, and the complexity of your spend base — not by which solution has the most features.

Spend Visibility and Analytics Infrastructure

A spend analytics capability consolidates accounts payable data, purchase order records, and contract information into a structured, categorized spend cube — giving leadership a single, accurate view of who is spending what, with which vendors, across which categories.

This is the non-negotiable first layer. Without it, every downstream sourcing or negotiation initiative operates on incomplete information. The most common failure mode is finance teams relying on general ledger summaries rather than invoice-level data, which obscures vendor duplication, tail spend leakage, and above-market pricing that only becomes visible when you analyze actual transaction records.

CPO Rising found that organizations using automated spend analysis are nearly twice as likely to identify sourcing opportunities — 87% vs. 47% for those without it. Each dollar placed under active procurement management typically yields 6%–12% in benefit within the first contract cycle.

| Attribute | Detail |

|---|---|

| Best For | Companies with fragmented AP data across multiple business units or ERP systems that lack real-time spend reporting |

| Key Capabilities | Spend categorization, vendor consolidation analysis, tail spend identification, category-level benchmarking |

| Expected Impact | Improved negotiation leverage, identification of duplicate vendors, and a baseline for all downstream sourcing initiatives |

Strategic Sourcing and Vendor Consolidation

Strategic sourcing applies structured competitive analysis — market benchmarking, RFP development, should-cost modeling, and supplier evaluation — to identify opportunities to reduce costs or improve terms with existing vendors, or to replace them competitively. Vendor consolidation reduces supplier count to increase volume leverage with fewer, more accountable partners.

Mid-market companies tend to accumulate far more vendors than they need. Decentralized buying over years creates a fragmented supplier base where no single relationship carries enough volume to drive meaningful negotiation. Higher spend concentration translates directly into pricing leverage, simpler AP management, and cleaner contract terms.

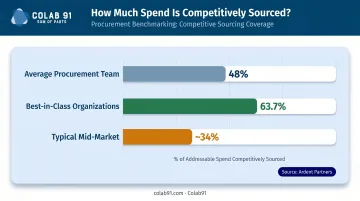

Ardent Partners found that the average procurement team competitively sources only 48% of total addressable spend, while best-in-class organizations reach 63.7%. For mid-market companies without structured sourcing programs, coverage is typically lower still.

| Attribute | Detail |

|---|---|

| Best For | Organizations with fragmented, high-vendor-count spend across categories like facilities, IT, logistics, or professional services |

| Key Capabilities | Competitive RFP processes, should-cost analysis, supplier scoring, contract standardization, volume rebate structures |

| Expected Impact | Direct cost reductions through competitive pricing, improved contract terms, and reduced administrative overhead from vendor management |

Category Management Programs

Category management organizes all third-party spend into defined categories — IT, facilities, professional services, logistics, and others — and assigns ownership of each to a responsible team with a dedicated sourcing and supplier strategy. The difference from ad-hoc sourcing events is continuity: category management creates a sustained savings pipeline rather than one-time wins.

For mid-market companies, the challenge is headcount. Running formal category teams across five or more spend categories requires dedicated resources that most mid-market procurement functions don't have. This is precisely why category management is well-suited to hybrid delivery models — where internal category owners set strategy and manage stakeholder relationships while external partners handle the analytical and market intelligence work.

Hackett Group research shows that top-performing Digital World Class procurement organizations generate 2.03x greater cost savings as a percentage of spend than their peers, and much of that performance advantage comes from structured, repeatable category discipline rather than one-off initiatives.

| Attribute | Detail |

|---|---|

| Best For | Mid-market companies with recurring, high-value spend in 3–5 categories where market dynamics and supplier relationships require ongoing management |

| Key Capabilities | Category strategy development, supplier relationship management, contract lifecycle management, market intelligence tracking |

| Expected Impact | Sustained year-over-year savings, improved supplier performance accountability, and reduced maverick spend within managed categories |

Offshore Procurement Capability Centers

Rather than building a large internal procurement or spend analytics team onshore, mid-market and PE-backed companies increasingly establish dedicated offshore teams — particularly in India — that handle spend analytics, sourcing support, contract management, and supplier data operations. These teams function as a strategic extension of the internal procurement function, not a generic outsourced service.

Everest Group estimates that mid-market firms account for approximately 45% of India's 1,760 Global Capability Centers, with mid-market GCC revenue projected to grow from $6.5B in 2024 to $7.5B–$7.8B by 2026. This is no longer just an enterprise strategy.

Colab91 was purpose-built for this use case. The firm's managing partners previously led Impendi's India operations — later acquired by Accenture — scaling that organization to 100+ practitioners serving PE sponsors including Carlyle Group, TPG, Elliott, and BC Partners. They bring that institutional experience directly to mid-market clients, helping companies establish India-based capability centers that handle procurement and spend analytics work at a fraction of the cost of equivalent onshore headcount.

Colab91's offshore teams are staffed with procurement and analytics domain experts, not generalists. Engagement models address entity ownership, IP rights, and scalability from the outset, and the teams are designed to grow with the client's needs rather than reset every contract cycle.

| Attribute | Detail |

|---|---|

| Best For | Mid-market and PE-backed companies that need to scale procurement and spend analytics capability rapidly without proportional onshore headcount growth |

| Key Capabilities | Spend data normalization, category analysis, sourcing event support, supplier benchmarking, contract compliance monitoring |

| Expected Impact | Significant reduction in total cost of procurement function while maintaining or improving delivery quality and analytical depth |

Automated E-Procurement and AP Tools

E-procurement platforms automate the purchase requisition, approval, purchase order, and invoice matching workflow. The result is a controlled buying channel that prevents maverick spend, reduces processing costs, and generates real-time spend data. AP automation tackles the manual invoice handling and payment error problem that creates both cost and compliance risk.

The mid-market automation gap is substantial. A 2025 CFO.com survey of 225 mid-market finance and accounting leaders found that only 4% had fully automated AP, while 38% of respondents took five or more days to process a single invoice. For context, Ardent Partners benchmarked the average cost to process a single invoice for mid-sized organizations at $11.57 — a number that adds up quickly at any meaningful transaction volume.

One important caveat: automation amplifies discipline but does not substitute for it. Companies that deploy e-procurement tools on top of broken approval workflows or inconsistent vendor master data will automate their problems rather than solve them. The right sequence is process clarity first, then technology to enforce it at scale.

| Attribute | Detail |

|---|---|

| Best For | Companies experiencing high transaction volume, inconsistent approval processes, or significant manual effort in invoice handling and PO creation |

| Key Capabilities | PO automation, three-way invoice matching, approval workflow management, spend dashboards, ERP integration |

| Expected Impact | Reduced processing costs per invoice, fewer payment errors, improved spend compliance, and faster procurement cycle times |

How to Choose the Right Spend Management Approach

The most common mistake mid-market companies make is selecting tools or programs based on features rather than organizational readiness. A sophisticated category management program adds no value if the spend data feeding it is uncategorized. An e-procurement platform creates friction rather than savings if approval workflows haven't been defined first.

Three Factors to Assess Before Committing

- Data maturity — Do you have reliable, categorized spend data at the invoice level? If not, analytics infrastructure comes first, before anything else.

- Available internal headcount — Who will operate the solution once it's implemented? Procurement software without procurement expertise is shelf-ware.

- Spend complexity — How many categories, vendors, and business units are involved? Higher complexity typically demands more structured delivery support, not just tools.

Matching Solutions to Business Outcomes

The right solution is the one that delivers measurable cost reduction relative to its total investment — including implementation time, internal resource commitment, and ongoing management costs.

For PE-backed companies, the timeline constraint is non-negotiable. Most investment horizons require demonstrable EBITDA improvement within 12–24 months of acquisition. Procurement typically represents 50%–80% of revenues, and a structured program addressing half that spend can deliver 8%–12% savings on the addressed portion — material EBITDA impact on any portfolio.

That math requires speed-to-value, which usually means augmenting internal capability rather than building it from scratch.

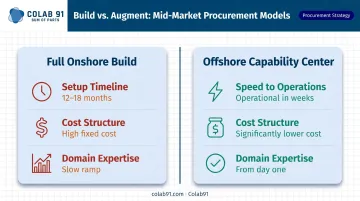

Build vs. Augment

Mid-market companies rarely need to choose between building entirely in-house or fully outsourcing. The most effective model is a hybrid: a small internal team sets strategy and manages stakeholder relationships, while specialized partners — including offshore capability centers — handle the analytical and operational execution.

For companies without an existing procurement function, the gap is even sharper:

- Full onshore build: 12–18 months to stand up, high fixed cost, domain expertise takes time to develop

- Offshore capability center: Operational in weeks, significantly lower cost, domain expertise embedded from day one

The offshore model doesn't just save money — it compresses the time between decision and measurable impact.

Conclusion

Spend management is a sustained capability, not a one-time initiative. Each sourcing cycle builds market knowledge. Each vendor consolidation expands leverage. Each analytics improvement sharpens the next negotiation — and the one after that.

Mid-market companies that invest early in spend visibility, category discipline, and scalable delivery models consistently outperform peers on margin and growth metrics. The ones that don't tend to fund that underperformance through vendor relationships that have never been challenged.

Start by assessing your current state honestly: Where is spend data incomplete? Where are vendors going unchallenged? Where is the team under-resourced to act on what they already know? Prioritize the gap that is costing you the most — that's where to start.

For mid-market and PE-backed companies looking to build or accelerate spend management capability without the cost and timeline of a large onshore team, Colab91 builds dedicated India-based teams with deep procurement and analytics expertise — the same model the leadership team used to scale Impendi's offshore operations to 100+ practitioners serving clients like Carlyle Group and TPG. It's a delivery structure purpose-built for mid-market economics. Contact Colab91 to discuss where your spend program needs the most support.

Frequently Asked Questions

What is spend management and why does it matter for mid-market companies?

Spend management is the structured process of gaining visibility into, controlling, and systematically reducing all third-party expenditure. Mid-market companies are particularly exposed because they often lack the dedicated procurement function that enterprise organizations rely on — meaning vendor relationships go unchallenged and spend data stays fragmented across business units.

What strategies can midsize companies use to reduce vendor costs?

The core levers are spend visibility and analytics, vendor consolidation, strategic sourcing through competitive RFPs, should-cost analysis, and ongoing contract compliance monitoring. The most effective programs integrate all five: clean data, structured sourcing processes, and the analytical talent to act on what the data reveals.

What automated tools can help control vendor spend for midsize companies?

E-procurement platforms, AP automation tools, and spend analytics software are the primary automation categories. These tools are most effective when paired with structured procurement processes — automation enforces process discipline, but only if that process is already defined. Define the workflow first; then let the tools reinforce it.

How do mid-market companies build a procurement function without a large internal team?

The offshore capability center model is the most practical alternative. Companies like Colab91 build India-based teams of procurement and analytics domain experts that function as a strategic extension of a small internal team — delivering enterprise-grade capability at mid-market economics, with faster setup timelines than hiring onshore.

How does spend analytics support cost reduction for mid-market organizations?

Spend analytics provides the foundational data layer, normalizing and categorizing all third-party spend to surface vendor consolidation opportunities, above-market pricing, tail spend leakage, and category-level savings targets. Without it, sourcing and negotiation initiatives work from incomplete information — and most organizations miss 15–30% of addressable savings as a result.