Companies delaying their India GCC strategy aren't saving time or money. They're losing ground to competitors who are already scaling innovation, analytics, and engineering teams from India. The question isn't whether to establish an India capability center — it's how quickly you can do it without getting it wrong.

TL;DR

- India hosts 1,760+ active GCCs employing 1.9M+ professionals and generating $64.6 billion in annual export revenue — the largest GCC ecosystem in the world

- Five structural advantages drive India's dominance: talent depth, cost-to-quality ratio, government policy support, digital infrastructure maturity, and a proven ecosystem

- GCCs have evolved from back-office cost centers into innovation hubs — 58% of India GCCs are now investing in agentic AI

- Mid-market and PE-backed companies are entering the GCC model at scale, with 480+ mid-market GCCs already operating in India as of FY2025

- Domain-specialist GCC partners consistently outperform generalist IT outsourcers on speed to productivity and long-term impact

India's GCC Dominance in 2026: The Scale That Speaks for Itself

The numbers behind India's GCC ecosystem are hard to argue with.

According to the NASSCOM-Zinnov India GCC Landscape Report, India had 1,760+ active GCCs as of FY2025, employing over 1.9 million professionals and generating $64.6 billion in annual export revenue — a 9.8% revenue CAGR over five years.

By 2030, that figure is projected to reach $99–105 billion, with the GCC count expanding to 2,100–2,200 centers and the workforce growing to 2.5–2.8 million professionals.

174 Fortune 500 companies — roughly 35% of the list — now operate 390+ GCCs in India, collectively employing 950,000+ professionals, according to data reported by ANSR and covered by The Hindu BusinessLine.

How India Compares to the Next-Best Alternatives

India's lead is structural — rooted in advantages that competing geographies simply don't replicate at scale. Poland serves primarily as a European nearshore hub. The Philippines remains anchored in BPO and voice services. Mexico functions as a US nearshore option for operational functions.

None of these markets replicate India's combination of:

- STEM graduate output at 2M+ annually

- Ecosystem maturity built over four decades

- Digital-first infrastructure at enterprise scale

- Cost-to-quality ratio that no comparable market matches

The result: India doesn't just lead the GCC market — it defines what a mature capability center ecosystem looks like.

| Geography | Primary Strength | GCC Suitability |

|---|---|---|

| India | Full-stack: engineering, analytics, operations | High — all functions |

| Poland | European nearshore, language coverage | Moderate — EU-focused |

| Philippines | BPO, voice, customer support | Limited — operational only |

| Mexico | US nearshore, manufacturing support | Limited — proximity play |

The 5 Reasons India Leads GCCs Globally in 2026

Unmatched Talent at Scale

India produces over 2 million STEM graduates annually, according to Invest India — with NASSCOM's 2022–23 digital talent report citing 2.5 million for that year. The country's overall tech workforce now exceeds 5 million professionals.

This isn't a narrow pipeline feeding one type of role. Indian STEM talent feeds:

- Software engineering and product development

- Data science and advanced analytics

- Procurement and strategic sourcing

- Finance transformation and FP&A

- R&D and engineering services

Zinnov's mid-market GCC research found that Indian GCCs anchor approximately 47% of global product management talent in India, with mid-market centers specifically showing a 1.5x higher share of DeepTech talent in AI, cloud, cybersecurity, and data science compared to non-mid-market GCCs.

Cost-to-Quality Advantage

India GCCs can deliver up to 60% savings compared to equivalent Western talent markets, according to Zinnov's analysis. The savings reflect a superior cost-to-value ratio: senior domain experts in procurement, analytics, and engineering at a fraction of onshore costs — not commoditized labor.

Tier-II Indian cities add another layer: talent costs run 20–30% lower than metro counterparts, with cities like Ahmedabad, Jaipur, Coimbatore, and Chandigarh contributing a growing digitally skilled workforce exceeding 100,000 professionals collectively.

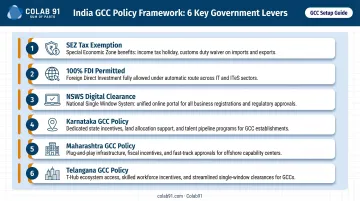

Government Policies and Regulatory Support

India's policy environment has reduced GCC setup friction significantly compared to five years ago. Key policy levers include:

- Special Economic Zones (SEZs): 100% income tax exemption on export income for the first five years, 50% for the next five, with continued concessions thereafter

- 100% FDI permitted under the automatic route across high-impact sectors

- National Single Window System (NSWS): Digital clearance platform for business approvals

- Karnataka GCC Policy 2024–29: The state hosts 500+ GCCs, accounts for 35% of India's GCC workforce, and targets 1,000 GCCs by 2029

- Maharashtra GCC Policy 2025: Fiscal and non-fiscal incentives for GCC units

- Telangana GCC Policy 2025–30: Targeting 15 million sq ft of Grade-A office space by 2030, with expansion into Tier-II cities like Warangal

State-level competition for GCC investment is intensifying, which translates directly into better incentive packages for companies setting up centers.

Digital-First Infrastructure

India's infrastructure maturity makes it purpose-built for data-intensive GCC operations:

- 469,000 5G base stations installed by February 2025, per government data

- Public cloud market reaching $10.9 billion in 2024, projected to hit $30.4 billion by 2029 at 22.6% CAGR, according to IDC research

- India's Digital Personal Data Protection Rules notified in November 2025, establishing a clear regulatory framework for data handling

- CERT-In cybersecurity directives requiring incident reporting within six hours, ensuring enterprise-grade compliance standards

A Mature, Proven Ecosystem

Four decades of GCC operations have built an ecosystem that newer geographies haven't had time to develop. Experienced talent pools, specialized service providers, academic partnerships, and startup networks are embedded in every major Indian city.

New GCCs benefit from this depth on day one:

- Faster ramp times driven by an established hiring market

- Lower execution risk through proven delivery infrastructure

- Ready access to GCC-specialized legal, HR, and real estate partners

From Cost Center to Innovation Engine: India's GCC Evolution

Where It Started

Texas Instruments established India's first software design center in Bengaluru in 1985 — the country's first multinational R&D presence. The 1990s and 2000s expanded that foundation into broad-based BPO and back-office operations, embedding GCC DNA into India's enterprise culture at scale.

That foundation now supports something far more sophisticated.

The Transformation

GCCs in India have shifted decisively from transactional functions to strategic ownership. According to the NASSCOM-Zinnov Landscape Report, 44% of India GCCs were classified as Portfolio Hubs in FY2024 — up from just 18% in 2013. Multi-functional GCCs grew 6x in five years. Engineering R&D-focused GCCs are expanding 1.3x faster than the overall GCC market.

In BFSI — one of the clearest examples of this evolution — India GCCs have moved from processing transactions to owning risk analytics, regulatory compliance automation, and AI-driven financial modeling. BFSI accounts for 21% of GCC sector adoption, followed by Retail/CPG at 14% and Healthcare at 12%.

AI as the 2026 Differentiator

The numbers on AI adoption within Indian GCCs are striking:

- 86% of Indian GCCs have adopted AI/ML

- 88% have implemented cybersecurity architectures

- 58% are actively investing in agentic AI workflows

- Two-thirds have created dedicated innovation teams, per EY's GCC Pulse Survey 2025

Agentic AI — systems that autonomously plan and execute workflows — is the capability separating genuine innovation centers from support hubs. India's GCCs aren't preparing for this shift — they're already executing it. And that capability is reshaping which GCC models actually deliver strategic value.

Domain-Specific GCCs: The Mid-Market Advantage

The most important structural shift for mid-market and PE-backed companies is the rise of domain-specific GCCs — centers built around deep functional expertise rather than generalist IT headcount.

A procurement and analytics GCC doesn't need 500 engineers. It needs 20–50 domain specialists who understand category management, spend analytics, supplier risk, and data infrastructure.

That team structure — lean, expert, embedded — is what separates a cost center from a capability center. Outcomes follow from specificity, not headcount.

Why Mid-Market and PE-Backed Companies Are Joining the GCC Wave

GCCs were historically the domain of Fortune 500 enterprises. By 2026, that has changed significantly.

480+ mid-market GCCs now operate in India, representing 27% of India's GCC landscape and employing 210,000+ professionals, according to the Zinnov-NASSCOM Mid-Market GCC Report. Critically, 35% of these centers were set up in the last two years — this is accelerating, not stabilizing.

Why PE-Backed Companies in Particular

PE sponsors and their portfolio companies face a specific constraint: value creation timelines are finite, and EBITDA improvement needs to be demonstrable within 12–24 months of platform investment. India GCCs address this directly.

Offshore capability centers in procurement, analytics, and finance can:

- Reduce operational costs by accessing cost-quality arbitrage that Western markets can't offer

- Accelerate analytical output — spend analysis, supplier benchmarking, and reporting that would take months onshore can be operationalized faster with dedicated offshore teams

- Scale without fixed cost burden — headcount can expand with the portfolio without proportional overhead growth

Zinnov's research consistently links offshore talent strategy to measurable EBITDA improvement — and for PE-backed businesses on compressed timelines, that connection is hard to ignore.

Choosing the Right Partner

The barrier to entry has fallen. What hasn't changed is the cost of getting the setup wrong. A generalist IT outsourcer will staff a team. A domain-specialist partner will design the operating model, recruit for functional fit, and manage governance from day one.

The Colab91 leadership team scaled Impendi's India operations to 100+ practitioners serving PE firms including Carlyle Group, TPG, Elliott, and BC Partners (prior to Accenture's acquisition). That track record is the foundation for what Colab91 does today: building procurement and analytics capability centers for mid-market and PE-backed companies.

What that looks like in practice:

- Operating model design tailored to each client's entity structure, IP rights, and strategic control requirements

- Domain-fit recruiting in strategic sourcing and spend analytics, not generalist staffing

- AI-powered tools (spend analytics, supplier risk management) embedded into the GCC's operating layer from day one

- Governance management from setup through steady-state operations

India's Top GCC Cities at a Glance

| City | GCC Strength | Market Share |

|---|---|---|

| Bengaluru | R&D, AI, software engineering, semiconductors | 34–44% of GCC leasing |

| Hyderabad | IT/ITeS, pharma, biotech, semiconductors | 20–25% of GCC leasing |

| NCR/Gurugram | Business innovation, procurement, analytics, BFSI | ~13% of GCC leasing |

| Pune | BFSI, automotive, engineering services, manufacturing | 15–20% of national activity |

| Mumbai | Financial services, banking, insurance | Tier-I hub |

| Chennai | Engineering, automotive, IT/ITeS | Tier-I hub |

India's GCC real estate hit a record 31 million sq ft of leasing in 2025, per JLL, with over 263 million sq ft of Grade-A GCC stock across the top seven cities.

Tier-II cities — Jaipur, Coimbatore, Chandigarh, Ahmedabad, Indore — are emerging as cost-effective expansion locations. Over 20% of new mid-market GCC expansions now occur in Tier-II and Tier-III cities, where talent costs run 20–30% below metro rates.

That geographic spread matters when it comes to city selection — because functional mandate should drive location, not habit. A procurement and analytics center has different talent requirements, infrastructure needs, and ecosystem access than a software engineering hub. Defaulting to Bengaluru without that analysis produces a setup, not a strategy.

Frequently Asked Questions

How do you set up a Global Capability Center in India?

Core setup steps include:

- Define strategic objectives and conduct a location/feasibility analysis

- Select your operating model (captive, hybrid, or managed)

- Build the legal and compliance framework

- Recruit domain talent and establish governance structures

Working with an experienced GCC partner accelerates setup and reduces execution risk.

What is a GCC and how is it different from outsourcing?

A GCC is a wholly owned offshore entity where the parent company retains full control over talent, IP, and processes. Outsourcing transfers delivery to a third-party vendor. That retained control is what makes GCCs strategic assets rather than transactional cost plays.

Why is India the top GCC destination compared to Poland or the Philippines?

India leads on talent scale (2M+ STEM graduates annually), ecosystem maturity (1,760+ active GCCs), cost-quality combination, and AI/digital readiness. No competing geography matches this combination at the same scale.

Can mid-market or PE-backed companies set up a GCC in India?

Yes. There are already 480+ mid-market GCCs operating in India with 210,000+ employees — well below the Fortune 500 threshold. Modular operating models and specialized partners have made setup accessible, and PE-backed firms in particular benefit from GCCs' ability to deliver measurable operational improvements within value creation timelines.

How much does it cost to set up a GCC in India, and what are the expected savings?

Setup costs vary by scale, operating model, and functional scope. Zinnov's analysis indicates that India GCCs can deliver up to 60% savings compared to equivalent Western markets. Model total cost of ownership — including setup, talent, infrastructure, and governance — rather than focusing only on initial setup costs.

How long does it take to operationalize a GCC in India?

Lean teams via managed or EOR structures can be operational within weeks; fully captive GCCs typically require 60–120 days for initial setup. Full operational maturity generally takes 6–12 months. An experienced GCC partner with prior build-out history can compress both timelines.