Introduction

For most of the past decade, PE returns looked deceptively simple: buy a business, add leverage, hold while multiples expanded, then sell. That playbook worked when debt was cheap and exit markets were liquid. It no longer does.

The numbers tell the story clearly. McKinsey's 2024 Global Private Markets Review found that leverage plus multiple expansion drove roughly 67% of realized buyout returns from 2010 to 2021. Since 2022, rising rates, compressed multiples, and a stalled exit market have closed that window — global buyout exit value fell 44% in 2023, and median hold periods stretched to 6.1 years.

The math now demands something harder: building genuine business value inside the portfolio company. Revenue growth, margin expansion, procurement discipline, capability upgrades — these aren't supplementary tactics anymore. They're the primary return engine.

What follows is a breakdown of the specific operational levers PE firms are pulling today — and where most portfolios are still leaving value on the table.

TL;DR

- Financial engineering alone can no longer carry PE returns — operational improvement is the core lever.

- Revenue growth and margin expansion are the two highest-impact value creation workstreams.

- Indirect procurement — representing 5–25% of company revenue — is consistently overlooked in most mid-market portfolios.

- Offshore domain-expert teams close capability gaps faster and cheaper than onshore hires or consultants.

- A structured Value Creation Plan — with clear KPIs, owners, and a monitoring cadence — separates execution from intention.

Why the Old PE Playbook Is No Longer Enough

US middle-market unitranche yields stayed above 12% in 2023, up from well under 7% just a few years earlier. Leverage in mid-market deals fell from 5.0x to 4.1x EBITDA. Median entry multiples contracted from 11.9x to 11.0x. Each of these shifts compresses returns on its own — in combination, they've rewritten the risk-return calculus for every deal underwritten today.

The practical consequence: sponsors can no longer underwrite a deal assuming debt will magnify returns or that a rising market will re-rate the exit multiple. Returns now have to be built, not assumed — which means PE firms need to be serious, earlier and more rigorously, about:

- Pricing discipline, customer retention, and sales productivity — not just topline growth

- Margin structure that distinguishes waste from spend that builds capability

- Operational infrastructure: data visibility, process automation, and reporting that actually informs decisions

- Talent — people with the right skills, in the right roles, incentivized to perform

Longer hold periods amplify both the cost of inaction and the reward for getting this right. A procurement saving realized in year one compounds over a six-year hold in ways a saving realized in year four never will.

Core Strategies for Portfolio Company Performance Improvement

Effective PE firms don't pick one lever — they run interconnected workstreams simultaneously. A 2024 KPMG survey of 500 PE leaders found 64% cite margin growth as their primary portfolio improvement strategy, with digital transformation and talent upgrades close behind.

Revenue Growth and Commercial Excellence

Revenue growth is the largest single contributor to PE value creation in realized buyout data. Bain's analysis of top-quartile deals attributes 35% of value creation to revenue growth — and the best operators treat this as an engineered outcome, not a market outcome.

The commercial levers that drive results:

- Pricing discipline: Most mid-market companies have never run a systematic pricing analysis. Even modest price optimization on the right SKUs or contracts can add 1–2 margin points without volume impact.

- Sales productivity: Shortening sales cycles, improving pipeline conversion, and reducing rep-level variance delivers growth without headcount additions.

- Customer retention: Churn is expensive. Reducing it through better account management and customer success investment has a higher ROI than new logo acquisition.

- Adjacent market entry: Adding a vertical, geography, or complementary service line can accelerate growth without requiring full-scale product development.

Margin Expansion and Cost Optimization

Revenue growth sets the ceiling; margin improvement determines what you keep. It's also faster to unlock and more directly controllable — the key is knowing which costs to cut and which to protect.

Blunt headcount reductions often destroy capability. A benchmark-driven approach is more durable: identify what the business spends versus what comparable businesses spend, isolate the categories where the gap represents waste rather than competitive investment, and eliminate those costs methodically.

Key cost workstreams in a PE margin improvement program:

- SG&A rationalization against revenue benchmarks

- Procurement and third-party spend optimization (covered in depth below)

- Process standardization to reduce rework and manual effort

- Footprint and real estate consolidation

Digital Transformation and Process Automation

Digital has shifted from long-horizon IT projects to near-term operational levers. According to PwC's Next in Private Equity Survey, 40% of portfolio company respondents named digitizing or automating business areas as their primary value-creation priority, with payback cycles now measured in months, not years.

The highest-ROI automation targets in mid-market PE portfolios:

- Financial reporting (still manual at most companies — 54% rely on email attachments for sponsor data requests)

- Spend data ingestion and categorization

- Operational dashboards that surface KPI variances in real time

Management and Leadership Upgrades

Spencer Stuart data shows 54% of PE portfolio companies had at least one new CEO between acquisition and exit. That frequency reflects a straightforward reality: the management team that ran a stable, owner-operated business often isn't the team that can execute a PE value creation plan.

Leadership upgrades should be planned during diligence, not triggered by underperformance. The most common gaps in mid-market acquisitions:

- CFO capability for PE-grade financial reporting and working capital management

- Chief Commercial Officer to drive pricing and sales transformation

- CPO or procurement leadership where third-party spend is a major cost driver

Procurement and Cost Optimization: The Underutilized Performance Lever

For most mid-market portfolio companies, indirect spend alone represents 5–25% of total revenue — yet it's frequently the last workstream to get structured attention post-acquisition. That's a significant oversight.

Alvarez & Marsal's analysis puts the EBITDA impact clearly: optimizing indirect procurement can deliver 0.4 to 2.0 percentage points of EBITDA margin improvement, within a total PE target range of 4–8 margin points over the hold period. Those numbers make procurement one of the most direct EBITDA conversion mechanisms available.

Why Strategic Sourcing Beats One-Off Cost Cutting

One-time renegotiations produce one-time savings. Strategic sourcing produces a compounding capability.

A structured procurement program involves:

- Spend visibility — Categorizing all third-party spend often reveals that 20% of suppliers account for 80% of addressable spend

- Supplier consolidation — Fewer suppliers per category increases negotiating leverage

- Contract renegotiation — Spend data and benchmarks replace assumptions at the table

- Category management — Repeatable processes sustain savings and surface new opportunities annually

The timing matters too. A&M's research on procurement benefit realization shows up to 20% of benefits can be captured in the first 100 days, with 70% by year one and full realization by 24 months. That timeline maps well to a PE hold period — provided the work starts at acquisition, not in year two.

The EBITDA Multiplier Effect

A recurring $1M reduction in indirect spend, at a 10–11x EBITDA multiple (McKinsey's reported 2023 median), translates to $10–11M in enterprise value. A $3M procurement improvement creates $30–33M at exit.

This is why PE sponsors with mature operating models treat procurement as a named workstream in the VCP, with dedicated resources and tracked EBITDA bridges.

Most mid-market portcos don't have the in-house bandwidth to build this function — and starting from scratch is slow. Colab91's leadership spent over 16 years scaling offshore procurement and spend analytics teams for marquee PE sponsors, including Carlyle Group, TPG, Elliott, and BC Partners, through Impendi's India operations (later acquired by Accenture).

Colab91 also offers AI-powered spend analytics, savings opportunity assessment, and supplier risk management tools built specifically for mid-market and PE portfolio company needs.

Closing the Capability Gap: Talent, Teams, and Flexible Operating Models

Mid-market portfolio companies are usually built for operational stability, not transformation velocity. When a PE sponsor acquires one, the existing team is often stretched thin on day-to-day management — leaving little bandwidth for the analytics, process redesign, and sourcing work the value creation plan demands.

Three Responses to a Capability Gap

| Approach | Speed | Cost | Durability |

|---|---|---|---|

| Hire onshore full-time | Slow (3–6+ months) | High | High |

| Engage consultants | Fast | Very high | Low (knowledge leaves) |

| Build offshore capability center | Moderate | Cost-efficient | High (embedded team) |

Each option has a place — but for PE sponsors optimizing for speed and EBITDA impact, offshore capability centers have become the default choice for functions like procurement analytics, financial reporting, and data science. The reason comes down to a meaningful structural difference: how a capability center is built versus what a standard BPO provides.

What Makes a Good Capability Center Different from a BPO

The distinction matters. A generic BPO provides headcount and process execution. A purpose-built capability center provides domain expertise and acts as a functional extension of the portfolio company's team.

Colab91's "Sum of Parts" approach is built on this distinction. Rather than replacing existing staff, it augments them: offshore procurement specialists and analytics experts who integrate with the onshore team, operate within the client's workflows, and build internal capability over time.

Engagement models are structured from the start to address entity ownership, IP rights, and strategic control — giving sponsors full visibility and flexibility as needs evolve.

This matters especially during transformation. A mid-market company doesn't need a 50-person offshore team on day one — it needs the right 5–10 specialists who can move quickly on spend analytics, reporting automation, or sourcing initiatives while the onshore team stays focused on operations.

Building and Executing a Value Creation Plan That Works

A Value Creation Plan is only as good as its execution architecture. Too many VCPs are built as investment committee presentations and never converted into operational reality.

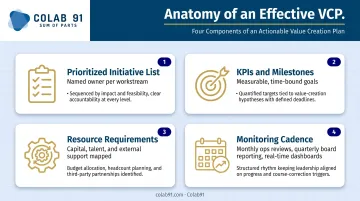

What an Effective VCP Contains

An actionable VCP has four components:

- Prioritized initiative list with a named owner for each workstream

- KPIs and measurable milestones — not "improve procurement" but "reduce indirect spend by $X by Q3"

- Resource requirements — capital, talent, and external support mapped to each initiative

- Monitoring cadence — monthly operational reviews, quarterly board reporting, real-time dashboards for leading indicators

The 80/20 principle applies directly here. Most PE portfolio companies have 20–30 potential improvement areas. The ones that actually move EBITDA are usually 5–7. A good VCP identifies those clearly and concentrates resources accordingly.

The First 100 Days Are Not Optional

The first 100 days post-acquisition set the operational trajectory. This is when spend baselines get established, management gaps get assessed, and quick-win initiatives get scoped. Delaying this work compresses the entire hold period, not just the first year.

KPMG's research notes that modern data infrastructure can reduce 100-day planning effort by 30%, which means the tools a sponsor deploys for data ingestion and reporting directly affect how quickly baselines are established and variance is detected.

Monitoring Is Where VCPs Die

The most common failure mode isn't a bad plan — it's a plan without accountability. Each review layer has a distinct job:

- Monthly operational reviews surface variance against KPI targets and trigger a response, not just a note

- Quarterly board reviews assess initiative progress against the EBITDA bridge, not just financial performance

- Real-time dashboards make problems visible before they compound

When these three layers work together, the VCP stays connected to actual operations. When they don't, initiative owners lose accountability and the EBITDA bridge becomes a best-case scenario rather than a tracked commitment.

Frequently Asked Questions

How do private equity firms improve portfolio company performance?

PE firms improve portfolio performance through a combination of operational levers — revenue growth, procurement optimization, management upgrades, and process automation — executed through a structured Value Creation Plan with clear KPIs and initiative owners. Best practice is to start this work within the first 100 days post-acquisition.

What common rules do PE firms use for portfolio company performance improvement?

The 80/20 rule (Pareto principle) helps prioritize which initiatives or spend categories deserve the most attention — typically 20% of areas drive 80% of the value opportunity.

The Rule of 72 is a quick mental model for estimating investment doubling time: divide 72 by the expected annual return to get approximate years to double.

What is a Value Creation Plan (VCP) in private equity?

A VCP is a structured operational blueprint created post-acquisition that outlines improvement initiatives, owners, timelines, and KPIs for growing revenue and expanding margins over the hold period. It should be built within the first 100 days and treated as a living document — not a static presentation.

What KPIs do PE firms typically track for portfolio company performance?

Common metrics include EBITDA and EBITDA margin, revenue growth rate, working capital efficiency, third-party spend as a percentage of revenue, employee productivity ratios, and customer retention rates — all measured against industry benchmarks and internal targets.

How long does it take to see operational improvements in a PE portfolio company?

Quick wins — procurement renegotiations, reporting automation, process fixes — can show measurable impact within 3–6 months. Structural improvements like management upgrades, digital transformation, and offshore capability center build-outs typically take 12–24 months to fully mature.

How can mid-market PE firms close capability gaps without large consulting spend?

Offshore capability centers — staffed with domain specialists in procurement, analytics, and finance — offer a cost-efficient alternative to onshore consulting. Unlike project-based engagements, dedicated offshore teams build durable internal capacity that compounds over the hold period rather than leaving when a project closes.